What is a monthly profit and loss statement

John Castro

Published Apr 23, 2026

A profit and loss statement provides businesses with a view of revenue, expenses, and income over a specified time frame. This step-by-step guide explains how to create a profit and loss statement.

What does a profit and loss statement tell you?

The P&L statement reveals the company’s realized profits or losses for the specified period of time by comparing total revenues to the company’s total costs and expenses. Over time it can show a company’s ability to increase its profit, either by reducing costs and expenses or increasing sales.

Why do you need a profit and loss statement?

P&L statements are important, because many companies are required by law or association membership to complete them. A P&L statement also helps a company’s management team (including its board of directors) to understand the business’s net income, which may be helpful in decision-making processes.

What is a profit and loss statement for self employed?

A P&L statement, also referred to as an income statement, measures your business revenue (income or sales) and expenses during a given time period. Put another way, a profit and loss statement tells you whether or not your business is making money.How do I prepare a profit and loss statement?

- Step 1: Calculate revenue. …

- Step 2: Calculate cost of goods sold. …

- Step 3: Subtract cost of goods sold from revenue to determine gross profit. …

- Step 4: Calculate operating expenses. …

- Step 5: Subtract operating expenses from gross profit to obtain operating profit.

Where do I find a profit and loss statement?

The P&L is found in the annual financial reports that all publicly traded companies are required by law to issue and distribute to shareholders. 1 Annual financial reports include a company’s P&L statement, balance sheet, and a statement of cash flow.

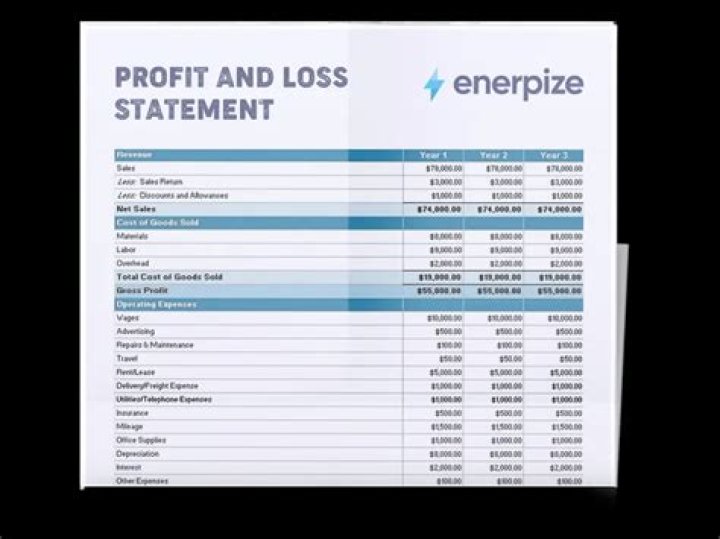

What is profit and loss statement example?

Total Revenue$1,000,000Less Cost of Goods Sold$378,700Gross Profit$621,300Gross Profit Margin62.13%Less Expenses

Do taxes go on profit and loss statement?

The income statement, or profit and loss statement, also lists expenses related to taxes. … It is listed as “taxes payable” and includes both long-term and short-term tax liabilities. When taxes are paid during the cash flow period reflected in the statement, then this change is shown as a decrease in taxes payable.Who needs a profit and loss statement?

The IRS requires sole proprietors to use Profit or Loss From Business (Sole Proprietorship) (Schedule C (Form 1040)), to report either income or loss from their businesses.

What's another name for profit and loss statement?An income statement or profit and loss account (also referred to as a profit and loss statement (P&L), statement of profit or loss, revenue statement, statement of financial performance, earnings statement, statement of earnings, operating statement, or statement of operations) is one of the financial statements of a …

Article first time published onIs income statement and P&L the same?

There is no difference between income statement and profit and loss. An income statement is often referred to as a P&L. The income statement is also known as statement of income or statement of operations. … income statement are actually the same, the terms will be used interchangeably throughout this article.

What is a profit and loss statement for a small business?

What is a profit and loss statement for small business? A profit and loss, P&L, or income statement shows your business’s revenue, expenses, costs, and net income over a specific period of time. You can generate a statement for any time period, but the most common time frames include monthly, quarterly, or annually.

Is it compulsory to prepare a profit and loss statement?

Why is preparing a profit and loss statement important? Preparing a profit and loss statement and reviewing it regularly will give you insight into area of the business where you are making money (or losing money).

Does a profit and loss statement need to be signed?

The P&L must be prepared and signed by a licensed accounting firm; a borrower prepared P&L is not eligible even if the borrower is an accountant and/or is employed by an accounting firm, and.

Why is profit and loss statement important to an entrepreneur?

The profit & loss account provides information about an enterprise’s income and expenses which result in net profit or net loss. It helps a businessman to evaluate the performance of an enterprise and provides a basis for forecasting future performance.

What is difference between profit and loss account?

Trading AccountProfit & Loss AccountThe trading account gives information related to trading activitiesIn Profit and Loss account you can determine the profit made by your business and loss sustained by the same

How does it differ from profit and loss account?

Key Differences Between Balance Sheet and Profit & Loss Account. … The Balance Sheet reveals the entity’s financial position, whereas the Profit & Loss account discloses the entity’s financial performance, i.e. profit earned or loss suffered by the business for the accounting period.

What type of account is profit and loss?

In accounting parlance, the Profit and Loss a/c is a Nominal Account. Every Account is prepared using the double effect in ‘Debit’ and ‘Credit. ‘ That means one of the accounts is debited, and the other is credited considering the golden rules of accounting.

Can a CPA prepare a profit and loss statement?

The primary functions of a CPA who performs an audit on a profit-&-loss statement are to generate an independent opinion of the income and expense items reported and to express his opinion in a written statement. CPAs who perform audits are third-party reviewers of profit and loss information.

How much does an audited profit and loss statement Cost?

Audited financial statements can cost you anywhere from $6,000 and can go up dramatically depending on the size and complexity of your company’s operations. Audits can also take anywhere from 3 weeks to a number of months to complete.