What are the five steps to revenue recognition

Ava Wright

Published Apr 17, 2026

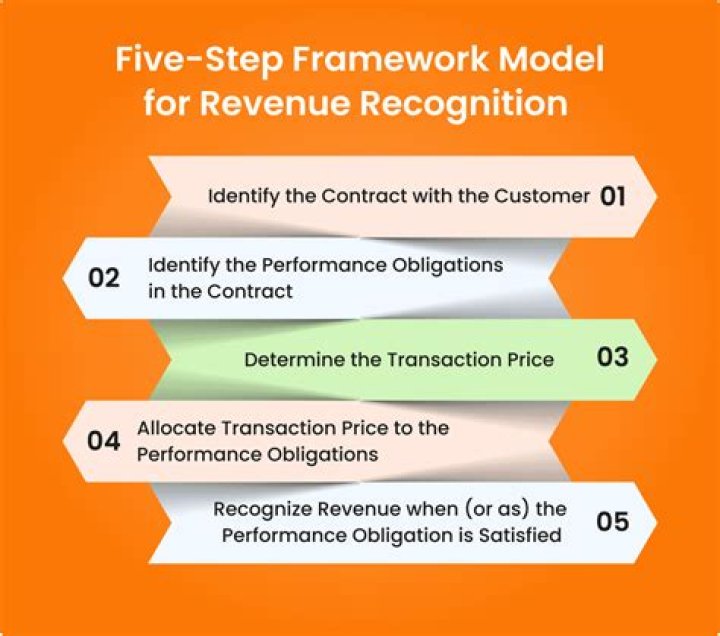

Step 1: Identify the Contract with a Customer. … Step 2: Identify the Performance Obligations. … Step 3: Determine the Transaction Price. … Step 4: Allocate the Transaction Price to the Performance Obligations. … Step 5: Recognize Revenue When or As Performance Obligations Are Satisfied.

What are the 5 steps of revenue recognition?

- Step 1 – Identify the Contract. …

- Step 2 – Identify Performance Obligations. …

- Step 3 – Determine the Transaction Price. …

- Step 4 – Allocate the Transaction Price. …

- Step 5 – Recognize Revenue.

What are the 5 steps of ASC 606?

- Identify the contract with a customer. …

- Identify the Performance Obligation in the contract. …

- Determine the transaction price. …

- Allocate the transaction price. …

- Recognize Revenue.

What is revenue recognition process?

The revenue recognition principle, a feature of accrual accounting, requires that revenues are recognized on the income statement in the period when realized and earned—not necessarily when cash is received. … Earned revenue accounts for goods or services that have been provided or performed, respectively.What five steps are needed to recognize revenue How are donations or contributions handled?

The five-step process involves identifying the customer and the contract, identifying the performance obligations, determining the transaction price, allocating the price to the performance obligations, and recognizing revenue when the performance obligations are met.

What is the first step in revenue recognition?

Identifying the contract or contracts with a customer is the first step in the new framework for determining revenue recognition. Under existing guidance, persuasive evidence of an arrangement typically does not exist until both parties have signed a contract.

What is the five step model in Ind AS 115?

Ind AS 115 prescribes five steps model to account for revenue: Identify the contract(s) with a customer. Identify the separate performance obligations in the contract. Determine the transaction price.

What are the types of revenue recognition?

- Sales-basis method. Under the sales-basis method, you can recognize revenue at the moment the sale is made. …

- Completed-Contract method. …

- Installment method. …

- Cost-recoverability method. …

- Percentage of completion method.

What are the four criteria for revenue recognition?

In this instance, revenue is recognized when all four of the traditional revenue recognition criteria are met: (1) the price can be determined, (2) collection is probable, (3) there is persuasive evidence of an arrangement, and (4) delivery has occurred.

What is revenue accounting?In accounting, revenue is the total amount of income generated by the sale of goods and services related to the primary operations of the business. Commercial revenue may also be referred to as sales or as turnover. … Profits or net income generally imply total revenue minus total expenses in a given period.

Article first time published onHow do you calculate revenue recognition?

- Revenue to be recognized = (Percentage of Work Completed in the given period) * (Total Contract Value)

- Percentage of work completed = (Total Expenses incurred on the project till the close of the accounting period. …

- Example 1 (Continued):

- Year 1.

- Year 2.

- Year 3.

- Year 4.

What is revenue recognition with example?

What is the Revenue Recognition Principle? The revenue recognition principle states that one should only record revenue when it has been earned, not when the related cash is collected. For example, a snow plowing service completes the plowing of a company’s parking lot for its standard fee of $100.

How do nonprofits recognize revenue?

The typical way most nonprofit organizations recognize revenue is to: Record income as cash. Invoice customers and donors and record that income as accounts receivable.

What is Indas 116?

Ind AS 116 defines a lease as a contract, or part of a contract, that conveys the right to use an asset (the underlying asset) for a period of time in exchange for consideration. … Ind AS 116 gives lessees optional exemptions for certain short-term leases and leases of low-value assets.

How will Recognise revenue in a construction company financing arrangement?

Once the outcome of the contract can be estimated reliably the contract costs and revenue will be recognised as revenue and expenses by reference to the stage of completion of the contracting activity at the end of the reporting period. This method is called the percentage of completion method.

What is IND 105?

The Ind AS 105: An entity shall classify a non-current asset (or disposal group) as held for sale if its carrying amount will be recovered principally through a sale transaction rather than through continuing use.

What is revenue recognition SAP?

Revenue recognition means that revenues can be posted in FI independently from the billing document (which normally posts to revenue accounts). This means that revenues can be posted before, during or after billing or a value that has already been billed can be distributed between various periods.

Why is revenue recognition principle needed?

The revenue recognition principle enables your business to show profit and loss accurately, since you will be recording revenue when it is earned, not when it is received. Using the revenue recognition principle also helps with financial projections; allowing your business to more accurately project future revenues.

What is recognition criteria?

The recognition criteria set out in this Statement specify the conditions under which an item which satisfies the definition of an element should be recognised (or included) in financial statements.

How many revenue recognition methods are there?

There are five primary methods a company can use for revenue recognition.

What is method of recognition?

a technique of measuring the amount of material learned or remembered by testing a person’s ability to later identify the content as having been encountered.

Which method of revenue recognition is most commonly used?

Sales-Basis Method Under the sales-basis approach, sales are recognized at the time of sale. This method works best when payment is assured, and all deliverables have been made. The sales-basis method is used for most types of retail sales.

Can you recognize revenue before invoicing?

Revenue Recognition is the accounting rule that defines revenue as an inflow of assets, not necessarily cash, in exchange for goods or services and requires the revenue to be recognized at the time, but not before, it is earned. You use revenue recognition to create G/L entries for income without generating invoices.

How do you check revenue?

A simple way to find sales revenue is by multiplying the number of sales and the sales price or average service price (Revenue = Sales x Average Price of Service or Sales Price).

How is revenue recognized under IFRS 15?

The core principle of IFRS 15 is that revenue is recognised when the goods or services are transferred to the customer, at the transaction price.

What is SaaS revenue recognition?

According to Investopedia, revenue recognition is a generally accepted accounting principle (GAAP) that identifies the specific conditions in which revenue is recognized and determines how to account for it. Simply stated, SaaS revenue recognition is the process of converting cash from bookings into revenue.

What is revenue recognition ASC 606?

ASC 606 is the new revenue recognition standard that affects all businesses that enter into contracts with customers to transfer goods or services – public, private and non-profit entities. Both public and privately held companies should be ASC 606 compliant now based on the 2017 and 2018 deadlines.

What is revenue in non profit?

Nonprofit organization revenue refers to the funds generated through its primary operations. It may include amounts collected through contributions, fundraising, membership, and service fees.

Can nonprofits have deferred revenue?

Unlike for-profit entities, nonprofits receive donations from businesses, individuals and government. When the donor specifies how or when the money should be used, the transaction is not recognized as a deferred revenue. … Because the situation is considered a donation, not related to sales or other type of revenue.

What is ind?

Indian Accounting Standard (abbreviated as Ind-AS) is the Accounting standard adopted by companies in India and issued under the supervision of Accounting Standards Board (ASB) which was constituted as a body in the year 1977. … MCA has to spell out the accounting standards applicable for companies in India.

Is IFRS 16 and Ind AS 116 same?

Ind AS 116 / IFRS 16 records the present value of all future lease payments as liability in the books of lessee as also a corresponding Right-of-use (ROU) asset. … The Right-of-use asset is depreciated over the lease term. Hence the rental cost now gets split into interest and depreciation.