How equilibrium price and output are determined by a firm under perfect competition

Mia Russell

Published Apr 10, 2026

In perfect competition, the price of a product is determined at a point at which the demand and supply curve intersect each other. This point is known as equilibrium point as well as the price is known as equilibrium price. In addition, at this point, the quantity demanded and supplied is called equilibrium quantity.

How price and output is determined under perfect competition in the long run?

Thus, for a perfectly competitive firm to be in equilibrium in the long run, price must equal marginal and average cost. Now when average cost curve is falling, marginal cost curve is below it, and when average cost curve is rising, marginal cost curve must be above it.

How does a firm in perfect competition determine its output to produce?

Based on its total revenue and total cost curves, a perfectly competitive firm—like the raspberry farm—can calculate the quantity of output that will provide the highest level of profit. At any given quantity, total revenue minus total cost will equal profit.

How the price is determined by the firm in perfect competition?

Price is determined by the intersection of market demand and market supply; individual firms do not have any influence on the market price in perfect competition. Once the market price has been determined by market supply and demand forces, individual firms become price takers.How is equilibrium price determined under perfect competition explain with the help of a diagram?

With perfect competition between buyers and sellers, an equilibrium price OP will be determined at which the quantity demanded is equal to the available supply. That is, equilibrium price will be established at the point where downward sloping demand curve DD intersects the vertical supply curve MS.

How does a firm reach equilibrium under perfect competition in short and long period?

Under perfect competition the marginal revenue is equal to price. So the formula MR=MC becomes P=MC. The individual firm, under perfect competition, maximises its net revenue by fixing output at the point where its marginal cost is equal to the market price of the product.

How the output is determined in short and long run competitive market?

The equilibrium price and output is determined at a point where the short-run marginal cost (SMC) equals marginal revenue (MR). Since costs differ in the short-run, a firm with lower unit costs will be earning only normal profits. In case, it is able to cover just the average variable cost, it incurs losses.

How is price determined under monopolistic competition?

, In monopolistic competition, firms make price/output decisions as if they were a monopoly. In other words, they will produce where marginal revenue equals marginal cost. … This monopolistically competitive firm will price its product like a monopolist: at the point at which marginal cost equals marginal revenue.How are price and output determined under monopoly?

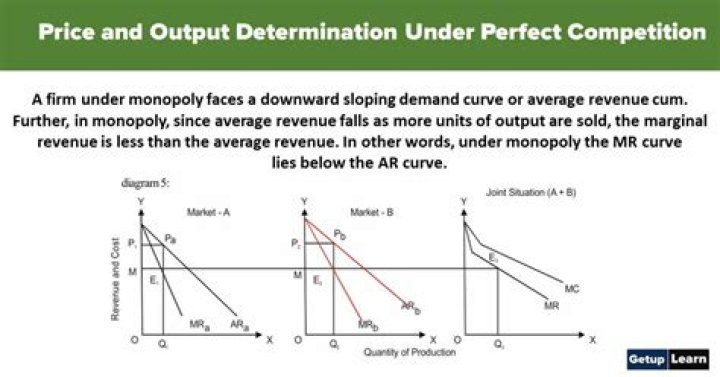

PRICE-OUTPUT DETERMINATION UNDER MONOPOLY: A firm under monopoly faces a downward sloping demand curve or average revenue curve. … In other words, under monopoly the MR curve lies below the AR curve. The Equilibrium level in monopoly is that level of output in which marginal revenue equals marginal cost.

What are the conditions of equilibrium of a firm under perfect competition?‘ Under conditions of perfect competition, the MR curve of a firm coincides with the AR curve. The MR curve is horizontal to the X- axis. Therefore, the firm is in equilibrium when MC=MR=AR (Price).

Article first time published onHow do firms determine price?

Since a perfectly competitive firm must accept the price for its output as determined by the product’s market demand and supply, it cannot choose the price it charges. This is already determined in the profit equation, and so the perfectly competitive firm can sell any number of units at exactly the same price.

What determines how a firm will produce its products?

The answer depends on the relationship between price and average total cost. If the price that a firm charges is higher than its average cost of production for that quantity produced, then the firm will earn profits.

How do you determine the quantity produced by the firm?

Key: To find the quantity the firm will produce in the long run recall that ATC = MC in the long run for the firm. 100/q + 5 + q = 5 + 2q q = 10 We can then figure out the market price by remembering that in the long run this firm’s MC = MR = P.

How does the equilibrium of a firm under perfect competition differ from monopoly?

A significant difference between the two is that while under perfect competition price equals marginal cost at the equilibrium output, under monopoly equilibrium price is greater than marginal cost. … Thus, under perfectly competitive equilibrium, price = MR = MC. In monopoly equilibrium, price > MC.

How is the equilibrium price of good determined explain with the help of demand and supply schedule and diagram?

Answer: The equilibrium price is the market price where the quantity of goods supplied is equal to the quantity of goods demanded. … To determine the equilibrium price, you have to figure out at what price the demand and supply curves intersect.

How are equilibrium price and output determined under it in short run?

Short-run price is determined by short-run equilibrium between demand and supply. Supply curve in the short run under perfect competition is a lateral summation of the short-run marginal cost curves of the firm.

How are price and output determined under monopolistic competition in the long run?

In monopolistic competition, profits are maximized at a point where marginal revenue is equal to marginal cost. … The price determined at this point is known as equilibrium price and the output produced at this point is called equilibrium output.

How equilibrium of a firm and industry is determined under monopolistic competition?

A Firm’s Short-Run Equilibrium under Monopolistic Competition. Under Monopolistic Competition, the revenue curves are downward sloping (like under Monopoly). This is because, in order to sell more, the firm has to decrease the price. … Therefore, they cannot compete away the super-normal profits of the firm.

How does a firm reach equilibrium?

A firm is said to be in equilibrium when its marginal cost is equal to marginal revenue and marginal cost curve cuts the marginal revenue curve from below. A firm in equilibrium enjoys supernormal profits if average revenue exceeds marginal cost.

What is perfect competition explain its characteristics and equilibrium of a firm under perfect competition?

Equilibrium in perfect competition is the point where market demands will be equal to market supply. A firm’s price will be determined at this point. In the short run, equilibrium will be affected by demand. In the long run, both demand and supply of a product will affect the equilibrium in perfect competition.

How is equilibrium price and quantity determined in a monopoly?

If the industry is a monopoly, then the equilibrium price and quantity is found by equating the marginal revenue curve for the monopolist with the marginal cost curve for the monopolist. The MR curve is MR = 1000 – 2Q while the MC curve is the supply curve. Thus, 1000 – 2Q = Q or Q = 333.3.

How are price and output determined under price discrimination?

The aim of monopolist is to increase total revenue and profit. … Under price discrimination, the monopolist will charge different prices in different sub-markets. Suppose, the monopolist has two different markets having different elasticity of demand.

What is price and output determination under perfect competition explain monopolistic competition?

Price-output determination under Monopolistic Competition: Equilibrium of a firm. In monopolistic competition, since the product is differentiated between firms, each firm does not have a perfectly elastic demand for its products. In such a market, all firms determine the price of their own products.

How do you calculate equilibrium price in perfect competition?

- Set quantity demanded equal to quantity supplied:

- Add 50P to both sides of the equation. You get.

- Add 100 to both sides of the equation. You get.

- Divide both sides of the equation by 200. You get P equals $2.00 per box. This is the equilibrium price.

How would one determine the equilibrium price and quantity?

- Use the supply function for quantity. You use the supply formula, Qs = x + yP, to find the supply line algebraically or on a graph. …

- Use the demand function for quantity. …

- Set the two quantities equal in terms of price. …

- Solve for the equilibrium price.

Is perfect competition a price taker?

A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells goods. … Perfect competition occurs when there are many sellers, there is easy entry and exiting of firms, products are identical from one seller to another, and sellers are price takers.

How do you determine if a firm will produce in the short run?

- Increase production if the marginal cost is less than the marginal revenue.

- Decrease production if marginal cost is greater than marginal revenue.

- Continue producing if average variable cost is less than price per unit.

What level of output does a firm produce?

a. What level of output will the firm produce? To maximize profits, the firm should set marginal revenue equal to marginal cost. Given the fact that this firm is operating in a competitive market, the market price it faces is equal to marginal revenue.

How do firms determine the optimal level of production?

As the objective of each perfectly competitive firm, they choose each of their output levels to maximize their profits. The key goal for a perfectly competitive firm in maximizing its profits is to calculate the optimal level of output at which its Marginal Cost (MC) = Market Price (P).

What are characteristics of perfect competition compare a firm equilibrium condition in perfect competition and imperfect competition?

What Is the Difference Between Perfect Competition and Imperfect Competition? While perfect competition is an idealized market structure in which equal and identical products are sold, imperfect competition can be found in monopolies and real-life examples.