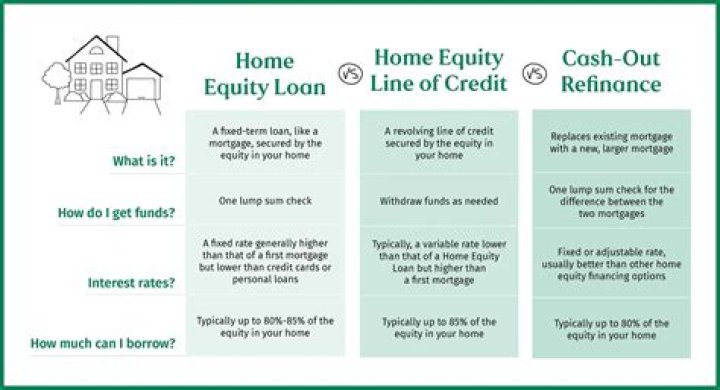

Can home equity line of credit interest be deducted in 2018

Olivia Zamora

Published Apr 17, 2026

For the tax years 2018 through 2025, you will not be able to deduct HELOCs. There are, however, a few exceptions. If you plan on taking this deduction, your loan must be used to “buy, build or substantially improve” the residence that secures the underlying loan.

Can you deduct home equity loan interest in 2018?

Beginning in 2018, taxpayers may only deduct interest on $750,000 of qualified residence loans. … However, if the taxpayer used the home equity loan proceeds for personal expenses, such as paying off student loans and credit cards, then the interest on the home equity loan would not be deductible.

What deductions can I claim for 2018?

- Mortgage-loan interest.

- Property tax.

- Self-employment deductions.

- Educator expense.

- Student loan interest.

- Relocation deductions.

- Charitable donations.

- Medical expenses.

Can home equity interest be written off?

With the passage of the Tax Cuts and Jobs Act of 2017, joint filers who took out their home equity loan after Dec. 15, 2017, can deduct interest on up to $750,000 worth of qualified loans, while separate filers can deduct the interest on up to $375,000.Is line of credit interest tax deductible in Canada?

Many people have a single line of credit that has been used both for investment purposes and for personal expenditures. The Canada Revenue Agency (CRA) considers interest on the investment portion tax deductible.

What is the 2021 standard deduction?

Filing StatusStandard Deduction 2021Standard Deduction 2022Single; Married Filing Separately$12,550$12,950Married Filing Jointly & Surviving Spouses$25,100$25,900Head of Household$18,800$19,400

Is home equity interest grandfathered?

Debt incurred on or before December 15, 2017 is grandfathered in under the old rules for home acquisition debt of $1 million or less. … It is still subject to the overall debt limits. Documentation and tracing will be important to determine the amount of deductible home equity interest.

Can you deduct interest on a second home?

Mortgage interest paid on a second residence used personally is deductible as long as the mortgage satisfies the same requirements for deductible interest as on a primary residence. … State and local real property taxes are generally deductible.Can you write off margin interest?

Yes, you can deduct margin interest provided it is paid in that year, and you also can only deduct interest expense on money borrowed to buy securities or investment property.

What kind of interest is not tax deductible?You cannot deduct interest on money borrowed to invest in passive activities, straddles, or tax-free securities. It’s best to keep loans for personal and investment use separate. If you borrow money for personal reasons and investment use, you must allocate the debt between the two.

Article first time published onWhat is grandfathered debt?

Definition of a grandfathered debt Grandfathered debt is a mortgage you took out on or before October 13, 1987.

Is a home equity loan considered taxable income?

First, the funds you receive through a home equity loan or home equity line of credit (HELOC) are not taxable as income – it’s borrowed money, not an increase your earnings. … This may be assessed by your state, county or municipality and are based on the loan amount. So the more you borrow, the higher the tax.

Is mortgage interest deduction grandfathered?

Homeowners with pre-existing mortgages were grandfathered in, meaning they could still deduct up interest on up to $1 million in mortgage debt if they received the loan before the 2017 cut-off. From 2017 onward, homeowners could only deduct interest on up to $750,000 in mortgage debt.

Is there an extra deduction for over 65 in 2021?

Taxpayers who are at least 65 years old or blind can claim an additional 2021 standard deduction of $1,350 ($1,700 if using the single or head of household filing status). For anyone who is both 65 and blind, the additional deduction amount is doubled.

How much of my Social Security is taxable in 2021?

For the 2021 tax year, single filers with a combined income of $25,000 to $34,000 must pay income taxes on up to 50% of their Social Security benefits. If your combined income was more than $34,000, you will pay taxes on up to 85% of your Social Security benefits.

Does Social Security benefits count as income?

Since 1935, the U.S. Social Security Administration has provided benefits to retired or disabled individuals and their family members. … While Social Security benefits are not counted as part of gross income, they are included in combined income, which the IRS uses to determine if benefits are taxable.

How much losses can you write off?

Your maximum net capital loss in any tax year is $3,000. The IRS limits your net loss to $3,000 (for individuals and married filing jointly) or $1,500 (for married filing separately). Any unused capital losses are rolled over to future years.

Can margin interest offset dividends?

Limits on Interest Deduction If you earn $10,000 from capital gains on your trades, in addition to interest income and ordinary dividends, then you can only deduct $10,000 in margin interest paid. You don’t add in “qualified” dividends, certain payouts which qualify for long-term capital gains rates.

Can I deduct credit card interest?

Credit card interest is never deductible for individuals, but it’s a different story when a business is involved. … However, the debt must be related to a trade or business activity. You can’t use your company credit card for personal expenses and then deduct the interest.

Why is my mortgage interest not deductible?

If the loan is not a secured debt on your home, it is considered a personal loan, and the interest you pay usually isn’t deductible. Your home mortgage must be secured by your main home or a second home. You can’t deduct interest on a mortgage for a third home, a fourth home, etc.

Can you deduct mortgage interest on a second home in 2021?

The mortgage interest deduction allows you to reduce your taxable income by the amount of money you’ve paid in mortgage interest during the year. … As noted, in general you can deduct the mortgage interest you paid during the tax year on the first $1 million of your mortgage debt for your primary home or a second home.

Does owning a second home help with taxes?

You can deduct property taxes on your second home, too. In fact, unlike the mortgage interest rule, you can deduct property taxes paid on any number of homes you own. However, beginning in 2018, the total of all state and local taxes deducted, including property taxes, is limited to $10,000 per tax return.

Is interest deducted before tax?

Interest is deducted from Earnings Before Interest and Taxes (EBIT) to arrive at Earnings Before Tax (EBT). EBIT is also known as Operating Profit, while EBT is also known as Pre-Tax Income or Pre-Tax Profit.

At what income level do you lose mortgage interest deduction?

There is an income threshold where once breached, every $100 over minimizes your mortgage interest deduction. That level is roughly $200,000 per individual and $400,000 per couple for 2021.

When can home equity line of credit points be deducted?

It depends. Interest paid on home equity loans and lines of credit is only deductible when you use the proceeds to buy, build or substantially improve your home that secures the loan.

How many homes can you deduct mortgage interest on?

The big deduction on a mortgage is the interest. You can deduct 100 percent of the interest on a mortgage on your primary home. You also can deduct all the interest on a second home, but never on more than two homes.

Can you still deduct mortgage interest in 2020?

The 2020 mortgage interest deduction Mortgage interest is still deductible, but with a few caveats: Taxpayers can deduct mortgage interest on up to $750,000 in principal.

What are the disadvantages of a home equity line of credit?

- HELOCs can come with a minimum withdrawal amount.

- There can be limitations to how you access the funds.

- There is a set withdraw period after which you cannot access any further funds.

- There can be fees associated with a HELOC.

- You can hurt your credit if you do not make payments on time.

- Harder to qualify right now.

Is interest on home loan tax deductible?

The mortgage interest deduction is a tax incentive for homeowners. This itemized deduction allows homeowners to count interest they pay on a loan related to building, purchasing or improving their primary home against their taxable income, lowering the amount of taxes they owe.

Does home equity count against capital gains?

The short answer to your question is that the home equity line of credit is unrelated to the potential capital gain or loss on the sale of your home. To calculate the gain or loss on the sale of your property, you take the gross sales price less your selling expenses to calculate the total amount realized.

Will paying off my mortgage raise red flags with the IRS?

Paying off a debt is not a “red flag”. Paying off a debt early is not a “red flag”. In fact, it’s barely relevant to income taxes at all.